You’re 55, 60, maybe 62. Retirement is on the horizon. And you’re asking yourself a question millions of Americans ask:

“Should I pay off my mortgage before I retire?”

Your parents would say yes. Dave Ramsey definitely says yes. Most financial gurus say yes.

But here’s what I’ve learned after 30 years in mortgages and financial coaching:

For many women over 50, paying off your mortgage early is one of the WORST financial moves you can make.

Not always. But often.

Let me show you why.

The Conventional Wisdom (And Why It May Be Wrong for You)

The traditional advice sounds logical:

“Retire debt-free. A paid-off house = security. No mortgage payment = lower expenses = easier retirement.”

And if you’re 70 with a paid-off house and plenty of retirement savings, that advice is FINE. It’s actually pretty solid.

But if you’re 50-65 and considering whether to throw extra money at your mortgage or invest it? The math tells a very different story.

Here’s what conventional wisdom DOESN’T account for:

- Opportunity cost (what you’re giving up by locking money in your house)

- Liquidity risk (being house-rich and cash-poor)

- Tax implications (losing your mortgage interest deduction)

- Your actual timeline (if you’re 55, you might have 30+ years ahead of you)

The Math That Changes Everything

Let’s run two scenarios. Same woman, same situation, two different choices.

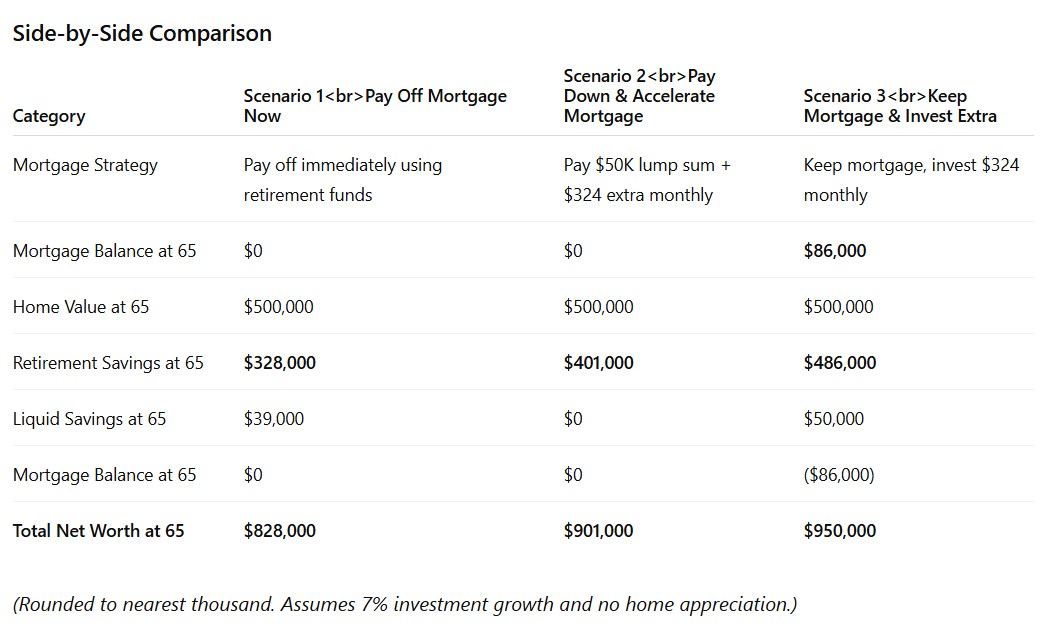

Meet Sarah. She’s 57 and would like to retire on her 65th birthday. She bought her home 15 years ago and financed $250,000.

- Today, the house is worth: $500,000

- Mortgage balance: $161,000

- Interest rate: 4%

- Monthly payment: $1193 (principal + interest)

- Retirement Savings: $250,000

- Extra liquid cash available: $50,000

- Years until retirement: 7

*All of these scenario’s below do not include earned interest.

SCENARIO 1: Sarah Pays Off Her Mortgage Early

Sarah takes $150,000 from her retirement savings and the $11,000 liquid cash saved and pays off her mortgage completely.

What happens:

- Mortgage is free and clear

- She has no monthly principal and interest payments

- She saves $1193/month in payments which she applies to retirement savings

- She’ll have the house paid off now, at age 58.

At age 65, Sarah has:

- A paid-off house worth $500,000

- Retirement savings: $328,000

- Liquid savings of $39,000

- Total net worth: $828,000 (includes interest estimated at 7%)

Not too shabby, right?

But wait. Let’s look at the alternative…

SCENARIO 2: Sarah Pays Down & Accelerates Her Mortgage

Sarah takes her $50,000 from liquid savings and pays down her mortgage.

What happens:

- New mortgage balance: $111,000

- New monthly payment to payoff in year 7 (by retirement) = $1517

- She is paying an additional $324/month in payments

- Because of the extra principal, she is not able to save more towards retirement.

- She’ll have the house paid off by age 65

At age 65, Sarah has:

- A paid-off house worth $500,000

- Retirement savings: $401,000

- Liquid savings: Zero

- Total net worth: $901,000 (plus interest earned over the duration)

This assumes she is comfortable paying the extra $324 per month and not dip into her retirement contributions.

This looks better than the full payoff except it leaves Sarah without any liquid savings for emergencies.

SCENARIO 3: Sarah Invests the $50,000 Instead

Sarah keeps her mortgage as-is. She decides as long as she still has income coming in, it makes sense. She invests the $50,000 in a diversified portfolio.

After weighing all her options, she decides to allocate that extra $324/month she would have made on the increased mortgage payments to her retirement planning, because it was do-able.

Assumptions:

- 7% average annual return (conservative historical average)

- 7 years until retirement

- Retirement early withdrawal penalty of 10% applied

At age 65, Sarah has:

- House worth $500,000 (still has mortgage of $140,000 remaining)

- Investment account: $50,000

- Retirement savings: $486,000 – she never took any money out.

- Total net worth: $1,036,000 – $86,000 mortgage = $950,000

Keeping the mortgage and investing the difference builds the highest net worth.

Here’s quick summary:

Scenario 1 creates peae of mind early, but results in the lowest long-term net worth, mainly due to pulling funds from retirement and paying a 10% penalty.

Scenario 2 balances emotional comfort and financial efficiency, producing the mid-range net worth at retirement.

Scenario 3 keeps liquidity and maximizes investment growth, landing the highest net worth while still carrying a modest mortgage into retirement (with just 8 years remaining)

But wait, there’s more! Here’s what this simple calculation DOESN’T show:

What the Numbers Don’t Tell You (But I Will)

-

Liquidity Matters MORE Than Net Worth

Scenario 1 (Paid-Off House):

- Sarah has $828K net worth

- But $500K is locked in her house (her home equity)

- She has $328K in retirement – also locked up, unless she withdraws with a penalty

- She has $39K in LIQUID assets, not bad but may not be enough

- If she needs money she has some liquidity but if there is a serious medical illness or condition, she has to pull out of retirement (with penalty) or get a HELOC (and be able to qualify).

Scenario 2 (Pay-Off Accelerated + Investments):

- Sarah has $901K net worth (a fair amount more)

- But she has $0K in LIQUID assets

- If she needs money, she cannot access it WITHOUT selling her home or depleting her retirement.

- She has NO Flexibility

Scenario 3 (Mortgage + Investments):

- Sarah has $950K net worth ( more)

- She maintained her retirement funds of $250K and kept it growing to now, $486K

- She has $50K in LIQUID assets

- If she needs money, she can access it WITHOUT selling her home or depleting her retirement.

- She has FLEXIBILITY

For women over 50, liquidity often matters MORE than net worth.

Why? Because life happens. Medical expenses. Helping aging parents. Supporting adult children. Opportunities you want to seize.

A paid-off house doesn’t help you with any of that.

-

Your Home Equity Is “Lazy Money”

When you pay off your mortgage early, you’re taking money that could be EARNING 7-10% per year and putting it into an asset that grows at… maybe 3-4% per year (home appreciation).

That’s opportunity cost.

Your home equity just SITS there. It doesn’t pay you dividends. It doesn’t generate income. It doesn’t compound.

It’s commonly referred to as LAZY MONEY.

Now, some people say, “But I’m saving 4% interest on my mortgage!”

True. But you’re also LOSING 7-10% potential gains in the market.

Net difference: 3-6% per year you’re leaving on the table.

Over 10-20 years? That’s $100,000-$300,000 in lost wealth.

If you itemize your taxes, your mortgage interest is tax-deductible.

That means your ACTUAL interest rate is lower than your stated rate.

Example:

- Mortgage rate: 4%

- Tax bracket: 24%

- Effective rate after deduction: 3.04%

So you’re borrowing money at 3% to invest at 7-10%. That’s smart leverage.

When you pay off your mortgage, you lose that deduction.

-

What If You Need the Money LATER?

Let’s say Sarah pays off her house at 65. At 72, she needs $50,000 for medical expenses.

Her options:

- Reverse mortgage (expensive, complicated)

- HELOC (might not qualify if her income is low in retirement)

- Sell the house (drastic)

- Pull from her retirement (not good, this is her only “nest egg” and she doesn’t have time to replenish it)

None of these are good.

But if she had kept her mortgage and invested the money? She’d have a sizable amount sitting in an account she could access ANYTIME.

I’ve seen this happen too often – a job loss, a major medical illness, serious emergencies – and the person can’t quality to tap into their equity.

Flexibility = security.

So When DOES It Make Sense to Pay Off Your Mortgage?

I’m not saying you should NEVER pay off your mortgage. There are situations where it makes perfect sense:

Pay Off Your Mortgage If:

You’re already 70+ and want peace of mind

- At this point, liquidity might matter less than simplicity

- You want to reduce monthly expenses

- You have plenty of other liquid assets

Your mortgage interest rate is HIGH (7%+)

- Paying off a 7% loan IS a guaranteed 7% return

- Hard to beat that without taking significant risk

You have anxiety about debt that affects your quality of life

- Mental health matters

- If the mortgage keeps you up at night, pay it off

- Peace of mind has value

You have MORE than enough retirement savings

- If you’ve got $2M in retirement accounts and a $150K mortgage, sure—pay it off

- You have plenty of liquidity elsewhere

Your house is your ONLY asset and you need to simplify

- If you don’t have significant retirement savings

- Keeping the house paid off protects your shelter

- Reduces risk of foreclosure

DON’T Pay Off Your Mortgage If:

You’re sacrificing retirement contributions

- Never skip your 401(k) match to pay down mortgage

- That’s leaving free money on the table

You’re depleting your emergency fund

- You need 6-12 months of expenses in cash

- Don’t lock it all in your house

You have high-interest debt

- Credit cards at 20%? PAY THOSE FIRST, please!

- Mortgage at 4% (or even 7%) is cheap money in this situation

You’re 10+ years from retirement

- You have TIME for investments to compound

- Don’t give up that growth

Your rate is below 5% and you’re a disciplined investor

- Investing the difference will likely net you more wealth

- Keep the cheap mortgage, grow your investments

The Real Question You Should Be Asking

Instead of “Should I pay off my mortgage?” ask this:

“What do I want my money to DO for me?”

This is such an important question – and most people skip it. Not because they are careless, but because they don’t know to ask it.

Do you want:

- Maximum flexibility? Keep the mortgage, invest the difference

- Maximum peace of mind? Pay it off

- Maximum wealth accumulation? Keep the mortgage, invest strategically

- Lower monthly expenses? Pay it off

- Access to capital? Keep the mortgage or refinance strategically

There’s no ONE right answer. There’s only the right answer FOR YOU.

My Recommendation for Most Women 50-65

If you’re in this age range and asking this question, here’s what I typically recommend:

OPTION 1: Keep Your Mortgage + Invest Aggressively

Best for:

- Women with 10+ years until retirement

- Those comfortable with investing

- Those with emergency funds in place

- Those who want to maximize wealth

Strategy:

- Keep making your regular mortgage payment (keeping your tax advantage)

- Invest extra money in other retirement vehicles that will create guaranteed income

- Let compound interest work in your favor

- Reassess at age 65-7

OPTION 2: The “Hybrid” Approach

Best for:

- Women who want SOME debt reduction but also want liquidity

- Those who are moderately risk-averse

- Those who want balance

Strategy:

- Make ONE extra mortgage payment per year (pays off loan ~7 years earlier)

- Invest the rest (and be consistent)

- Gives you progress on both fronts without sacrificing too much

OPTION 3: Wait Until 5 Years Before Retirement, Then Decide

Best for:

- Women who aren’t sure yet

- Those who want to see how their investments perform

- Those who want maximum flexibility NOW

Strategy:

- Keep the mortgage as-is for now

- Invest extra money (and keep at it consistently)

- At age 60-65, ask yourself these questions and evaluate:

- How much do you have in investments?

- What’s your income need in retirement?

- What’s your mortgage balance?

- What feels right emotionally?

THEN decide whether to pay it off

Real Example: What I Am Doing…

I’ll be honest with you. I’m 64. I have a mortgage.

And I’m keeping it.

Why?

Because my interest rate is very low (under 4%). My investments are earning more than that. And I value having liquid assets more than I value a paid-off house.

I know the math. And I know MY priorities. And sadly, I’ve seen too many emergencies happen to people with paid off homes. And it is more stress than I’m willing to take on.

Your priorities might be different. And that’s okay.

The key is making an INFORMED decision… not just following what everyone says you “should” do.

What to Do Next

If you’re wrestling with this question, here’s what I recommend:

STEP 1: Run YOUR Numbers

Don’t guess. Calculate this:

- What’s your mortgage balance?

- What’s your interest rate?

- How much extra could you put toward it each month?

- How much could you invest instead?

- What would each scenario look like in 10 years? 20 years?

STEP 2: Consider Your Goals

What matters MORE to you:

- Peace of mind (paid-off house)?

- Flexibility (liquid investments)?

- Maximum wealth accumulation?

- Lower monthly expenses?

Write all this down. Writing it down helps your brain process and work towards making decisions. Come back to it tomorrow, and the next day, until you feel you have clarity over your numbers and what’s important to you most.

STEP 3: Talk to Someone Who Gets It

Not just ANY financial advisor. Someone who:

- Understands mortgages AND investments

- Won’t push you toward one answer because they earn commission on it

- Will run YOUR numbers based on YOUR situation

I offer free 30-minute strategy sessions where we look at YOUR situation – not generic advice, but YOUR numbers, YOUR timeline, YOUR goals.

No pressure. No sales pitch. Just clarity.

Schedule Your Free Mortgage Strategy Session

The Bottom Line

Should you pay off your mortgage before retirement?

Maybe. Maybe not.

It depends on:

- Your current interest rate

- Your timeline until retirement

- Your other assets (such as your retirement plan)

- Your risk tolerance

- Your goals

- Your need for liquidity

But here’s what I know for sure:

Blindly following “pay off all debt” advice can cost you hundreds of thousands of dollars in lost wealth.

So don’t do what Dave Ramsey says. Don’t do what your parents did.

Do what makes sense for YOUR situation.

And if you’re not sure what that is? Let’s talk.

Because 30 years of doing this has taught me one thing:

The right strategy isn’t the one that sounds good. It’s the one that actually WORKS for your life.

Ready to figure out YOUR mortgage strategy?

Schedule a free consultation: Book Your Session

Let’s make sure your money is working FOR you and with you… not against you.

Related Articles: