My friend Linda turned 53 last month. She makes $94,000 a year. She’s been paying off the same credit card for seven years.

“I pay $180 every month,” she told me over coffee. “It just never seems to go down.”

I asked one question: “What’s the interest rate?”

She didn’t know.

Turns out? 23.99%.

That $180 monthly payment? Only $37 was touching her balance. The other $143 was pure interest. She’d paid over $12,000 in interest alone – and still owed $6,200.

Here’s what shocked me most: Linda is brilliant. She manages a team of twenty. She raised two kids on her own. She can negotiate million-dollar contracts without blinking.

But nobody ever taught her how debt actually works.

And she’s not alone.

According to a 2024 Federal Reserve study, 62% of women over 50 carry credit card debt month to month, and 47% don’t know the interest rates they’re paying (source).

These are the most common money mistakes women 50+ make – and they’re all fixable. Maybe you’re thinking, “That’s not me. I’ve got this handled.”

Good. But I bet you know a woman who doesn’t. Your sister. Your friend. Your coworker who keeps saying she’s “working on it.”

These five mistakes cost women over 50 an average of $47,000 in lost wealth over ten years. If that got your attention, I understand – it got mine as well. We’ll walk through each one… and exactly how to fix them…in the next few minutes.

Mistake #1: The Money Mistake Women 50+ Make with Debt Order

The problem: Most women pay whichever bill is due next, or whichever balance feels most urgent. This keeps them stuck in an endless cycle.

The hidden cost: You could be paying off debt 40% slower than necessary – and paying thousands more in interest.

Here’s what most financial advisors won’t tell you: The order you pay off debt matters more than how much you pay.

The Math Nobody Shows You

Let’s say you have three debts:

- Credit card A: $3,000 balance, 18% interest, $90 minimum

- Credit card B: $6,000 balance, 24% interest, $180 minimum

- Car loan: $8,000 balance, 5% interest, $310 minimum

Most women pay minimums on everything and throw extra money at whichever feels most pressing.

The cost? Years of extra payments.

According to research from Harvard Business School, strategic debt payoff (focusing on high-interest or quick-win debts first) reduces total payoff time by an average of 15 months and saves $4,200 in interest for the median debtor (source).

Linda’s Twist

Remember Linda with the $6,200 credit card at 23.99%?

When we mapped out her debts, she had five accounts. She’d been spreading $400/month across all of them equally because it “felt fair.”

We redirected that $400 using the debt avalanche method (highest interest first).

- Timeline before: 6.5 years to debt-free

- Timeline after: 2.8 years to debt-free

- Interest saved: $8,900

Same money. Different order. She nearly cried when she saw the numbers.

“I thought I was being responsible by paying on everything. I was actually making it harder.” — Linda M

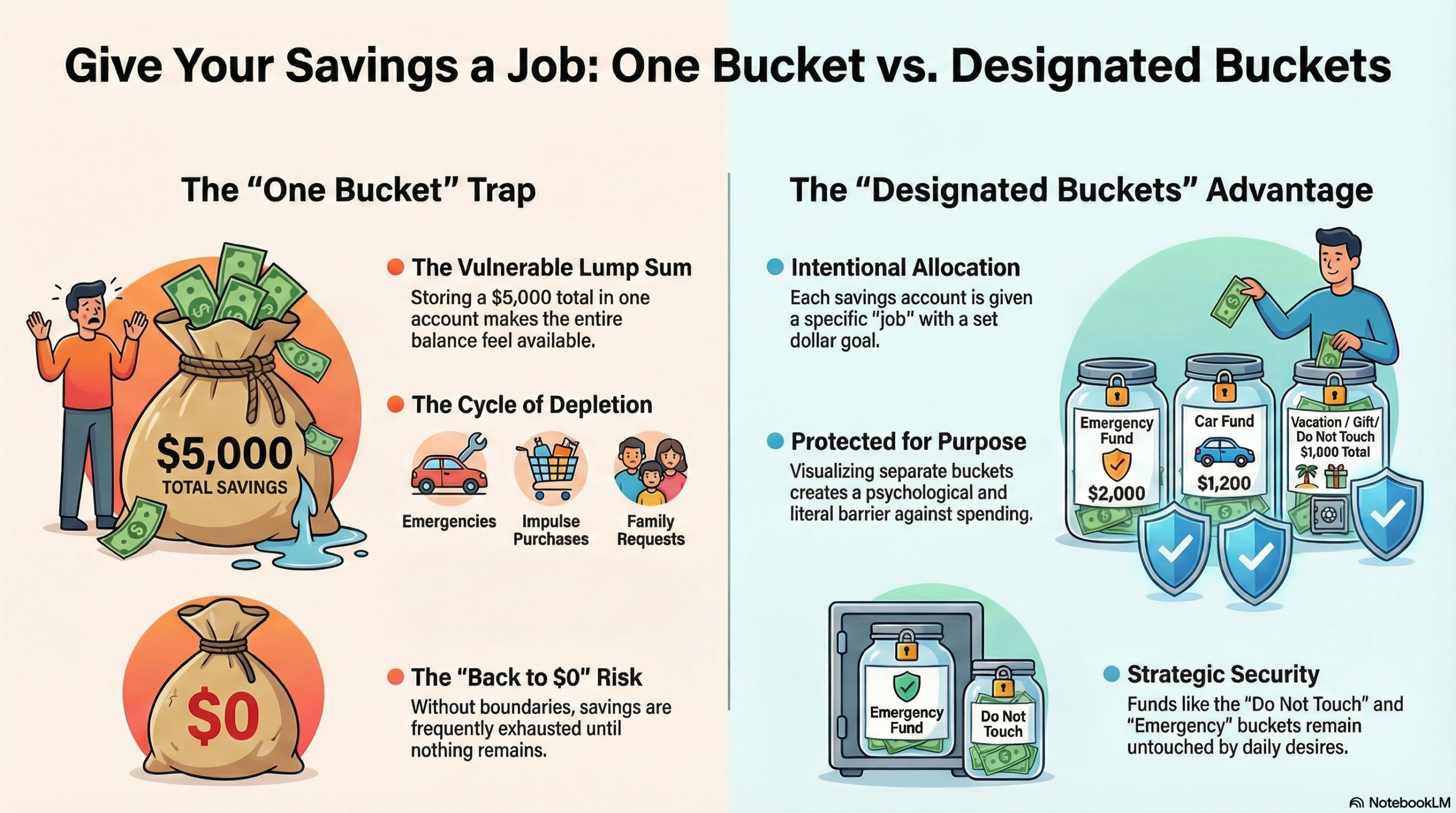

Mistake #2 Treating All Savings Goals the Same

The problem: One of the biggest money mistakes women 50+ make is often lumping everything into one “savings” bucket—emergency fund, vacation, retirement, future car, home repairs.

The hidden cost: When money isn’t designated for a specific purpose, it gets spent on whatever crisis pops up first. Then you’re back at zero.

A 2023 study by the National Bureau of Economic Research found that people with designated savings accounts (emergency separate from goals separate from retirement) save 34% more over five years than those with general savings (source).

Why This Matters at 50+

At this stage of life, you need multiple types of stability:

Immediate access: Emergency fund (car breaks down, medical bill, job loss)

Short-term goals: Vacation, holiday spending, new appliance

Medium-term: Car replacement, home improvements, helping adult kids

Long-term: Retirement, healthcare costs, legacy

When everything sits in one account labeled “savings,” your brain doesn’t protect it. It’s just money. And money gets spent.

The Fix: Bucket Your Money

Open separate accounts:

- Emergency Fund (3-6 months expenses)

- Opportunity Fund (for things you want, not need)

- Upcoming Expenses (insurance, property tax, etc.)

- Do Not Touch (retirement contributions, long-term goals)

Even if you start with $200 in each, the psychological shift is massive. Your emergency fund isn’t for Christmas shopping. Your vacation fund isn’t for car repairs.

Mistake #3: Waiting to “Feel Ready” to Tackle Finances

The problem: Women over 50 often delay financial clarity because they’re waiting to feel less overwhelmed, less busy, less scared.

The hidden cost: Every month you wait costs you in stress, missed opportunities, and compounding problems.

A Northwestern Mutual study found that Americans who delay financial planning for “just one more year” lose an average of $82,500 in retirement wealth due to missed investment growth and delayed debt payoff (source).

The Procrastination Tax

Here’s what waiting actually costs:

Scenario: Woman at 52 with $15,000 credit card debt at 19% interest

If she starts strategic payoff today: Debt-free in 3.2 years, total interest paid: $5,100

If she waits “one more year” to get organized: Debt-free in 4.2 years, total interest paid: $7,800

Cost of waiting: $2,700 + one year of stress

Sarah’s Story: The Two-Hour Shift

Sarah, 58, kept saying she’d “deal with her finances this weekend.” For three years.

Then her daughter got engaged. Sarah wanted to help with the wedding but had no idea if she could afford it.

We spent two hours mapping her complete financial picture. That’s it. One Saturday morning.

Here’s what she discovered:

- She had $8,200 in forgotten accounts (old 401k, savings bonds)

- She was paying for three subscriptions she didn’t use ($67/month)

- Her debt payoff was going to take 8 years at her current pace—but only 3.5 years with strategic reordering

The twist: She could afford to contribute $5,000 to her daughter’s wedding if she used the forgotten accounts strategically and stopped the subscription bleed. This is why knowing which money mistakes women 50+ make matters so much.

“I spent three years avoiding this because it felt too big,” she said. “It took two hours. And now I can breathe.”

Mistake #4: Keeping Emotional Debt Instead of Strategic Debt

The problem: Women prioritize paying off debt based on guilt (“I should never have gotten this card”) instead of math.

The hidden cost: Your emotions are costing you thousands in unnecessary interest.

The Guilt Tax

I see this constantly: A woman will aggressively pay off a $2,000 debt at 8% because it reminds her of a painful divorce or failed business, while carrying $8,000 at 22% that she ignores because “it’s just always been there.”

Debt doesn’t care about your feelings. Interest doesn’t either.

Here’s the truth: The debt that makes you feel the worst is rarely the debt costing you the most.

Real Numbers

Emotional approach:

Pay off $2,000 loan at 8% first → Annual interest cost: $160

Keep $8,000 credit card at 22% → Annual interest cost: $1,760

Strategic approach:

Attack $8,000 at 22% first → Annual interest cost drops by $1,760

Then handle $2,000 at 8% → Small delay, massive savings

That’s $1,600/year you’re handing to credit card companies to manage your guilt.

The Permission Slip

You are allowed to be strategic even when it doesn’t feel good.

Paying off the “shameful” debt might make you feel better temporarily. But staying in debt longer costs you more – in dollars and in freedom

“Pay what costs you most, not what hurts you most.”

Mistake #5: Not Knowing Your Debt Freedom Date

The problem: Most women have no idea when they’ll actually be debt-free. They’re paying monthly but can’t see the finish line.

The hidden cost: Without a target date, there’s no urgency. No plan. No hope. Just endless payments.

According to a 2024 study by the Consumer Financial Protection Bureau, people who calculate their “debt freedom date” pay off debt 23% faster than those who don’t, simply because visibility creates motivation.

Why the Date Matters

When you know your debt freedom date, everything changes.

Instead of: “I’ll always have debt”

You think: “I’ll be debt-free by October 2027”

Instead of: “This is hopeless”

You think: “22 months. I can do this.”

The date gives you a countdown. And countdowns create momentum.

How to Find Your Date

You don’t need fancy software. You need five pieces of information:

- Total debt balance

- Interest rates for each debt

- Minimum payments

- Extra money you can throw at debt each month

- Payoff order (avalanche or snowball method)

Plug those into a debt payoff calculator (or use the Debt Slayer System to map it precisely).

Suddenly, you go from “drowning” to “I have a plan.”

Homeownership Bonus

Here’s something most women don’t realize: Getting debt-free (or close to it) is often the key to qualifying for better rates on everything—including mortgages if homeownership is in your future.

According to Freddie Mac, improving your debt-to-income ratio by paying off high-interest debt can qualify you for mortgage rates 0.5-1% lower, saving tens of thousands over the life of a loan. Debt to income ratio explained here on Investopedia. (source).

But even if you never buy a home, knowing your debt freedom date gives you something priceless: hope with a deadline.

How to Fix These Money Mistakes Women 50+ Make (This Week)

You don’t have to fix everything today. Just take one focused step.

✓ Pull your debt list

Write down every debt: balances, interest rates, minimum payments. Don’t judge. Just list.

✓ Calculate one thing

Pick your highest-interest debt. Calculate how long it would take to pay off if you added just $50 extra per month. Use a free calculator here.

✓ Open one designated savings account

Start with emergency fund. Even if you can only put $25 in it. The account exists. That’s the win.

✓ Find your debt freedom date

Use a payoff calculator or the Debt Slayer System to see your actual timeline. Get the date on your calendar.

✓ Share this with one woman who needs it

Know someone stuck in the debt cycle? Send her this. It might be the permission she needs to start.

The Real Cost of These 5 Money Mistakes

Let’s add up what these money mistakes women 50+ make actually cost.

Mistake #1 (wrong payoff order): Costs 15 extra months + $4,200 in interest

Mistake #2 (no designated savings): Costs 34% less wealth accumulated

Mistake #3 (waiting to start): Costs $2,700 + one year of stress

Mistake #4 (emotional vs strategic debt): Costs $1,600/year in extra interest

Mistake #5 (no debt freedom date): Costs 23% slower payoff

Total potential cost over 5-10 years: $35,000-$50,000 in lost wealth and unnecessary interest.

That’s not a typo.

These aren’t small mistakes. They’re wealth-killers.

But here’s the good news: Every single one is fixable.

You don’t need to be perfect. You don’t need to earn more. You don’t need to deprive yourself or live on rice and beans.

You just need to pay your debt in the right order. Know your numbers. Have a plan.

That’s it.

From Mistakes to Momentum

If you recognized yourself in any of these mistakes, you’re not alone. And you’re not behind.

You’re exactly where you need to be to make a change.

Linda (the woman from the beginning) is now 18 months into her debt payoff plan. She’s eliminated three credit cards completely. Her debt freedom date is June 2026.

Sarah helped her daughter with the wedding, stress-free, because she knew exactly what she could afford.

They didn’t become different people. They just got clear on the numbers and followed a system.

You can too.

Maybe you’re not making these mistakes. But if you know someone who is—your friend who’s been “working on debt” for years, your sister who avoids looking at her accounts, your coworker who seems stressed every time money comes up—send this to her.

Because the women who need this most are often the ones who won’t ask for help.

But they’ll read something you share.

Ready to see your debt freedom date?

The Debt Slayer System maps your exact payoff timeline, shows you which debts to attack first, and calculates how much you’ll save in interest. No judgment. Just math that works.

Get Debt Slayer for $49 → Get Started Today

Elizabeth Rose is a financial educator who helps women build clarity, confidence, and freedom with their money. With 30+ years of experience, she specializes in helping women who’ve carried everything alone finally create systems that work.