Margaret owned her home for twelve years. She paid $287,000 for it. She sold it last year for $420,000.

Her friend told her she’d owe massive capital gains taxes. Margaret panicked. She started calculating 15% of $133,000 profit. That’s $19,950 she’d never see again.

Except she didn’t owe a penny.

Not one dollar in capital gains tax. Why? Because she knew one tax strategy for homeowners over 50 that her friend didn’t: the $250,000 capital gains exclusion.

Here’s the truth nobody tells you about tax strategies for homeowners over 50: You’re probably overpaying by thousands because you don’t know what you’re entitled to claim.

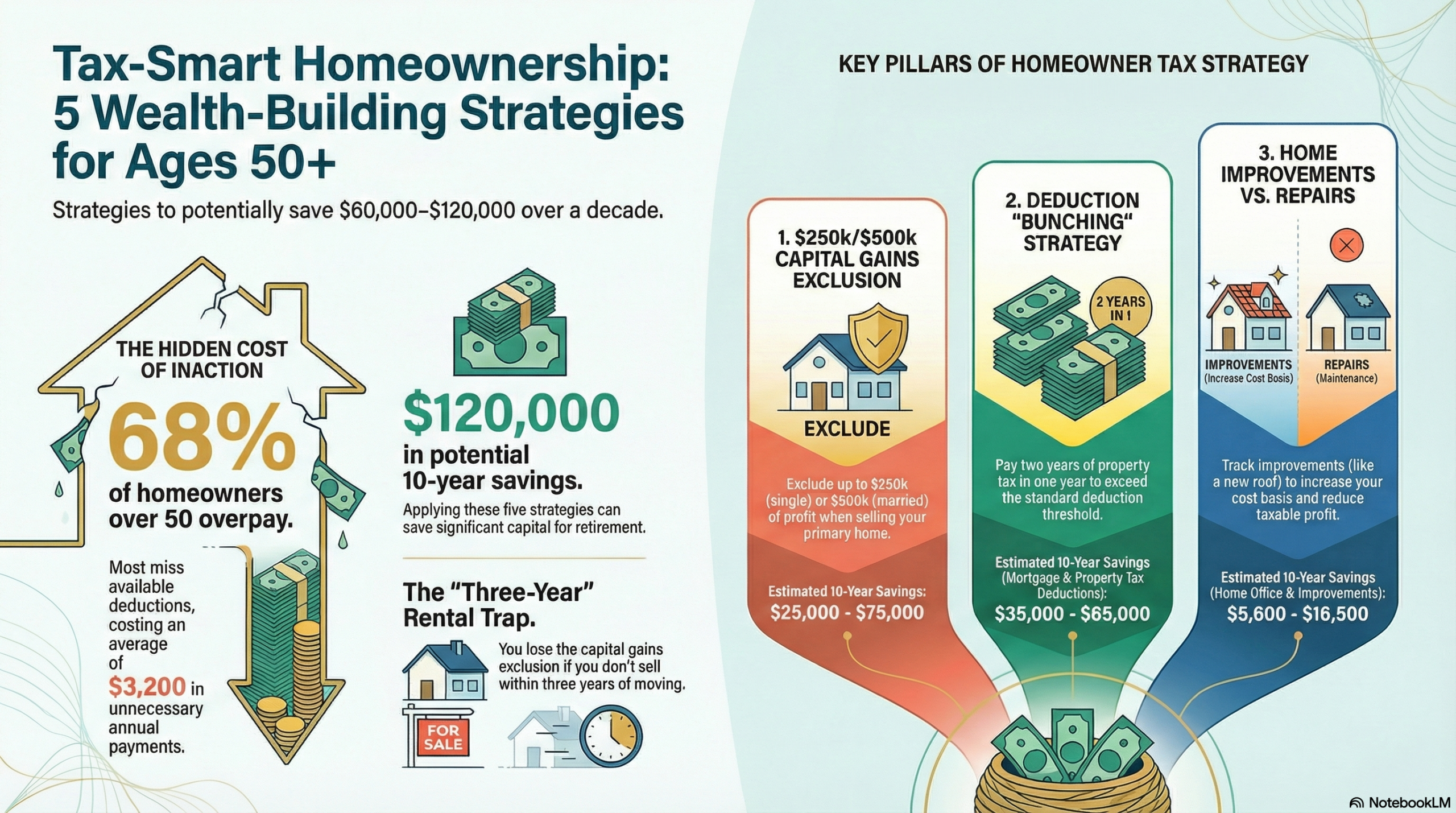

According to the National Association of Realtors, 68% of homeowners over 50 don’t maximize their available tax deductions, costing them an average of $3,200 annually in unnecessary tax payments. (source)

Maybe you’re thinking, “I have an accountant. They handle this.”

Great. But do they know about the specific deductions available when you’re over 50? Do they know which home improvements are deductible and which aren’t? Do they understand how downsizing affects your tax strategy?

Most don’t. And what they don’t know costs you money.

We’re going to walk through five tax strategies for homeowners over 50 that could save you $10,000-$30,000 over the next decade. Real strategies. Real savings. No fluff.

Strategy #1: Maximize Your Capital Gains Exclusion Before It’s Too Late

The rule: If you’ve lived in your home as your primary residence for at least two of the last five years, you can exclude up to $250,000 in profit from capital gains tax (or $500,000 if married filing jointly). Irs.gov/taxtopics/

Why this matters for Homeowners 50+: You might be thinking about downsizing, moving closer to family, or relocating for retirement. Understanding this exclusion could save you tens of thousands.

How It Actually Works

Let’s say you bought your home for $200,000. Today it’s worth $425,000. Your profit: $225,000.

Without the exclusion: You’d owe capital gains tax on $225,000. At 15% rate, that’s $33,750 in taxes.

With the exclusion: You pay $0. The entire $225,000 profit is yours.

The Timing Trap Women Fall Into

Here’s where women over 50 make expensive mistakes:

Mistake: Moving in with a partner or family member while keeping your home as a rental, thinking you’ll sell “eventually.”

The cost: If you don’t sell within three years of moving out, you lose the exclusion. That $225,000 tax-free profit? Now fully taxable.

Real numbers: A client moved in with her daughter to help with grandkids. She kept her home, rented it out for three years, then sold. She lost the $250,000 exclusion and owed $37,500 in capital gains tax she could have avoided.

“I didn’t know there was a clock ticking. I thought I could sell whenever I was ready.” — Patricia S., 61

How to Use This Strategically

If you’re planning to sell within 5 years:

- Make sure you’ve lived there at least 2 of those 5 years

- Track your residency carefully if you split time between homes

- Don’t convert to rental too early

If you’re downsizing:

- Understand you can use this exclusion multiple times in your life

- Just not more than once every two years

If you’re married:

- Coordinate timing if one spouse hasn’t lived there the full two years

- Understand the $500,000 joint exclusion requirements

This alone can save you $25,000-$75,000 in taxes. That’s real money that stays in your pocket.

Strategy #2: Deduct Mortgage Interest (Even in Your 50s and Beyond)

One of the best tax strategies for homeowners over 50 is maximizing your mortgage interest deduction – yes, even if you’re approaching retirement.

The rule: You can deduct interest paid on mortgage debt up to $750,000 ($1 million if the mortgage originated before December 15, 2017).

Why Women Over 50 Miss This

Many women assume: “I should pay off my house before retirement. Debt is bad.”

Sometimes that’s true. But sometimes keeping a mortgage is smarter tax strategy.

Here’s the math:

Let’s say you have a $200,000 mortgage at 6% interest. You’re paying about $12,000/year in interest.

If you’re in the 24% tax bracket:

- Mortgage interest deduction saves you: $2,880/year in taxes

- Over 10 years: $28,800 in tax savings

If you pay off the mortgage:

- Tax savings: $0

- That $200,000 is now locked in your home (not liquid, not growing)

When Keeping Your Mortgage Makes Sense

Scenario 1: Your money earns more elsewhere

If your mortgage rate is 6% but you can earn 8-10% in investments, keeping the mortgage while investing your cash might build more wealth.

Scenario 2: You need liquidity

At 50+, having accessible cash matters more than having a paid-off house. Emergencies happen. Opportunities arise. Equity in your home doesn’t help with either.

Scenario 3: The tax deduction is valuable

If you’re in a higher tax bracket (24%+), the mortgage interest deduction is worth thousands annually.

The Downsizing Decision

Here’s a strategy most women don’t consider:

When you downsize from a $400,000 home to a $280,000 home, you have options:

Option A: Pay cash for new home (no mortgage, no interest deduction)

Option B: Put 20% down ($56,000), keep a small mortgage, invest the remaining $224,000

Over 10 years:

- Option A tax savings: $0

- Option B tax deduction value: ~$15,000 (depending on rate and bracket)

- Option B investment growth potential: $60,000-$90,000 (at 6-8% annual return)

The difference: $75,000-$105,000 in additional wealth by keeping a strategic mortgage.

I’m not saying debt is always good. I’m saying strategic debt with tax advantages can build more wealth than being mortgage-free.

Strategy #3: Leverage Property Tax Deductions (Especially in High-Tax States)

The rule: You can deduct up to $10,000 in state and local taxes (SALT), which includes property taxes.

Why this matters: If you live in a high-property-tax state (New Jersey, Illinois, Texas, California, New York), this deduction saves you thousands.

The Numbers

National average property tax: $2,800/year

High-tax states: $6,000-$12,000/year

If you’re paying $8,000/year in property taxes and you’re in the 24% tax bracket:

- Without deduction: You pay full freight

- With deduction: Saves you $1,920/year in federal taxes

Over 10 years: $19,200 in tax savings

The Strategy Women Over 50 Miss

Many women bunch their deductions strategically in alternating years to maximize the benefit.

How it works:

Instead of paying property taxes in December every year, you:

- Pay two years of property tax in one calendar year (December + January)

- Take the standard deduction the next year

- Repeat

This lets you exceed the standard deduction threshold in high-deduction years and still benefit from the standard deduction in low-deduction years.

Result: More total tax savings over a two-year period.

Strategy #4: Deduct Home Office Expenses (If You’re Self-Employed)

This is one of the most overlooked tax strategies for homeowners over 50, especially for women who are:

- Self-employed

- Running a side business

- Consulting post-retirement

- Operating a small business from home

The rule: If you use part of your home exclusively and regularly for business, you can deduct a portion of housing expenses.

What You Can Deduct

Direct expenses (100% deductible):

- Painting/repairs in your office space

- Office furniture and equipment

- Business-specific upgrades

Indirect expenses (proportional to office size):

- Mortgage interest (additional deduction beyond standard)

- Property taxes (additional beyond SALT cap)

- Utilities

- Home insurance

- Repairs and maintenance

- Depreciation

Real Numbers

If your home is 2,000 sq ft and your office is 200 sq ft (10% of home):

Annual housing costs:

- Mortgage interest: $12,000

- Property tax: $6,000

- Utilities: $3,600

- Insurance: $1,800

- Maintenance: $2,400

- Total: $25,800

Home office deduction (10%): $2,580/year

Tax savings (24% bracket): $619/year

Over 10 years: $6,190 in tax savings

Plus depreciation deduction (approximately $1,800/year) adds another $432/year in tax savings.

Total annual tax benefit: ~$1,000

The Simplified Option

Don’t want to track every expense? Use the simplified method:

$5 per square foot, up to 300 square feet

200 sq ft office = $1,000 deduction annually

Tax savings (24% bracket): $240/year

Not as much as the detailed method, but zero paperwork hassle.

Strategy #5: Make Home Improvements That Add Value AND Tax Benefits

Not all home improvements are created equal when it comes to tax strategies for homeowners over 50.

The rule: Most improvements aren’t immediately deductible, BUT they increase your cost basis—which reduces capital gains when you sell.

What Counts as an Improvement

Adds value, prolongs life, or adapts to new use:

- Room additions

- New roof

- HVAC system replacement

- Kitchen/bathroom remodel

- Deck or patio addition

- Energy-efficient upgrades (solar panels, windows, insulation)

- Accessibility modifications (ramps, grab bars, wider doorways)

Does NOT count (these are repairs/maintenance):

- Painting (unless part of larger remodel)

- Fixing a leak

- Replacing broken appliances

- Routine maintenance

How This Saves You Money

Remember Margaret from the beginning? She bought her home for $287,000 and sold for $420,000 (profit: $133,000).

But she’d made improvements:

- New roof: $18,000

- Kitchen remodel: $35,000

- HVAC replacement: $12,000

- Bathroom updates: $15,000

- Total improvements: $80,000

Her adjusted cost basis: $287,000 + $80,000 = $367,000

Her taxable profit: $420,000 – $367,000 = $53,000

Even if she HADN’T qualified for the $250,000 exclusion, she’d only owe taxes on $53,000 instead of $133,000.

Tax saved: 15% of $80,000 = $12,000

Track every improvement. Save every receipt. It’s worth thousands when you sell.

Energy-Efficient Tax Credits (Bonus)

Through 2032, you can claim:

- 30% tax credit on solar panel installation (up to project cost)

- Up to $1,200/year for energy-efficient windows, doors, insulation

- Up to $2,000 for heat pumps, heat pump water heaters

Example: Install $20,000 solar system → Get $6,000 tax credit (not deduction—actual dollar-for-dollar reduction in taxes owed).

Quick-Start Tax Strategy Checklist

✓ Track your residency dates (for capital gains exclusion)

✓ Keep detailed records of all home improvements (receipts, invoices, before/after photos)

✓ Calculate whether keeping your mortgage makes tax sense (compare interest deduction value to payoff benefits)

✓ If self-employed, measure your office space (and start tracking home office expenses)

✓ Maximize property tax deduction (consider bunching strategy if near standard deduction threshold)

✓ Research energy-efficient tax credits before making upgrades (30% back is substantial)

✓ Consult a tax professional who understands homeowner 50+ strategies (not all CPAs specialize in this)

What This Actually Saves You

Let’s add up the potential savings from these tax strategies for homeowners over 50:

Strategy #1 (Capital gains exclusion): Save $25,000-$75,000 on home sale

Strategy #2 (Mortgage interest deduction): Save $2,000-$4,000/year

Strategy #3 (Property tax deduction): Save $1,500-$2,500/year

Strategy #4 (Home office deduction): Save $600-$1,500/year if self-employed

Strategy #5 (Home improvements reduce capital gains): Save $5,000-$15,000 on sale

Over 10 years: $60,000-$120,000 in tax savings

That’s not an exaggeration. Those are real numbers from real strategies available to you right now.

Why Women Over 50 Especially Need These Strategies

Here’s what most financial advice doesn’t acknowledge:

Women over 50 are often in a wealth-building sweet spot for homeownership but a vulnerable spot for retirement security.

You likely:

- Own a home with substantial equity

- Are earning peak income (or recently retired)

- Have 10-20+ years before full retirement

- Need to maximize every dollar for retirement security

These tax strategies for homeowners over 50 aren’t just about saving money. They’re about building the retirement cushion you need.

Every $3,000 saved in taxes today is $3,000 you can invest for retirement.

Compounded at 7% over 15 years? That $3,000 becomes $8,276.

Tax savings aren’t just savings. They’re wealth-building opportunities.

The Bottom Line

Margaret saved $19,950 in capital gains taxes because she knew one strategy.

You can save $60,000-$120,000 over the next decade by using all five.

These tax strategies for homeowners over 50 aren’t loopholes. They’re legitimate deductions and exclusions written into tax code specifically for homeowners.

But they only work if you know about them. And if you use them strategically.

You don’t need to become a tax expert. You just need to know what questions to ask and what records to keep.

Because the difference between knowing and not knowing?

It’s tens of thousands of dollars that either stays in your pocket or goes to the IRS.

Choose wisely

Elizabeth Rose is a financial educator specializing in helping women over 50 build wealth and security through strategic homeownership. With 30+ years of experience in real estate, mortgage and financial services, she helps women keep more of what they earn.